When you’re betting in a prediction market, be it an election, a rate decision, or a football game, the biggest question isn’t what to bet on, but how much. Bet too little and your wins don’t count. Bet too much and one bad call wipes you out.

That’s where the Kelly criterion comes in. It’s a tool designed to find your “sweet spot” bet size so you can grow your bankroll over time without gambling it all away.

In this guide, we’ll cover the following points:

- Definition of the Kelly criterion

- Step-by-step application

- Common pitfalls to avoid

What is the Kelly criterion

Before we jump into the practical steps, let’s understand what the Kelly criterion actually does.

Definition

The Kelly criterion is a simple money management rule created by John L. Kelly Jr. in the 1950s. Think of it as a guide to staking, telling you how big your next bet should be, to maximize your long-term growth while managing risk.

At its core, the Kelly approach says this: “Bet more when the odds are in your favor, and less (or nothing) when they’re not.” Professional gamblers, sports bettors and investors have been using it for decades to strike a balance between boldness and caution.

Key components

To use Kelly, you need two numbers:

- The market probability: This is what the current price says. If a “Yes” share costs 60 cents, the market thinks there is a 60% chance of it happening.

- Your estimated probability: This is what you think the real odds are based on your research. If you think it’s actually an 80% chance, you have an edge.

Simple formula

The simple version of the formula is:

f* = (bp − q) / b

Where:

- f* = fraction of your bankroll to bet

- b = net odds received (decimal odds − 1)

- p = your estimated probability of winning

- q = 1 − p

You don’t need to memorize the full formula, just focus on the logic: if your estimated probability of an event is higher than the market’s implied probability, Kelly helps you decide how much of your bankroll to risk.

Let’s say there’s a market on whether an election candidate will win. The market is giving odds that imply a 50% chance, but after researching polls and trends, you believe the true probability is closer to 60%.

That edge, the difference between your belief and the market’s estimate, is what Kelly uses to size your bet. The greater the edge, the bigger your optimal stake. If the numbers were reversed, you believed the true odds were 45% but the market said 50%, you’d bet zero, because there’s no advantage.

Importance of the Kelly criterion

The magic of the Kelly criterion is compounding. By controlling your risk and betting proportionally to your advantage, you let winners grow your bankroll and keep losers from crushing it. Over many bets, this balance leads to better, steadier results than either “go hard or go home” or over-cautious minimum stakes.

How to use Kelly in prediction markets

Now that you understand the logic, let’s turn it into a process you can actually use.

Step-by-step application

Using Kelly in a prediction market isn’t complicated once you know the steps. Here’s the practical way to do it:

- Estimate the true probability of an event.

Do your own work, study data and read analysis to form a reasoned estimate. You don’t need perfect accuracy, but the more objective you are, the better. - Compare your probability to the market’s.

The market’s implied probability is in the price. For example, if a contract trades at 50¢ per share for “Yes,” that means the crowd thinks there’s a 50% chance. - Find your edge.

Subtract the market’s probability from your own. Continuing the election example: 60% – 50% = 10% edge. - Use Kelly to estimate bet size.

You can think of the Kelly fraction as roughly equal to “edge divided by odds.” In this case, betting 10% of your bankroll would be close to full Kelly, meaning an optimal stake for maximum growth if your estimate is accurate. But that’s a big “if.” - Adjust, review, repeat.

As your bankroll grows or shrinks, adapt your bet sizes. If your predictions turn out off-base, scale down even more. Kelly isn’t fixed, it evolves as your confidence and capital do.

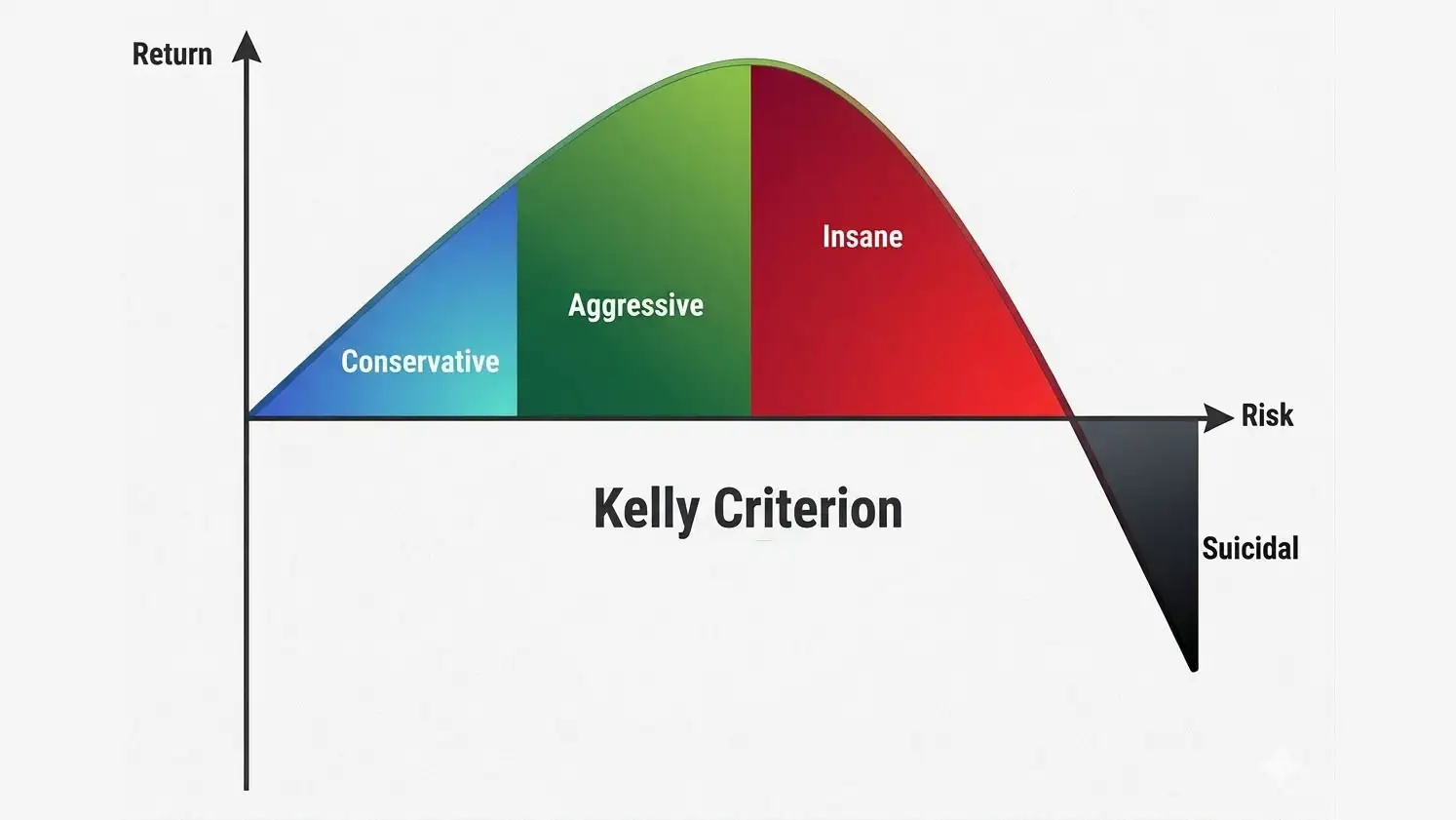

The golden rule: use fractional Kelly

No one’s forecasts are perfect, especially in prediction markets where probabilities shift fast. Most seasoned bettors use half-Kelly or even quarter-Kelly to stay disciplined. For instance, instead of betting 10% of your total bankroll, you might stake 5% or 2.5% instead. Fractional Kelly tones down the risk while keeping you in the game for the long haul.

A practical example

Imagine you’re betting on whether the US Fed will cut rates next month.

- The market is currently trading at 40.

- Your analysis gives a 55% chance.

That’s a 15% edge. If you were to apply full Kelly, you might risk around 15% of your bankroll, but that’s not wise in highly uncertain markets. Using half-Kelly, you’d instead bet about 7%. It’s enough to meaningfully benefit from your edge but not enough to ruin you if your call is wrong. Over time, this approach compounds your returns while minimizing big drawdowns.

What are common pitfalls to avoid

Even the smartest system can backfire if used carelessly, and as you start applying Kelly, watch out for a few common traps.

- Overconfidence: It’s easy to overestimate your edge. Always sanity-check your probabilities and be conservative when they’re uncertain.

- Ignoring costs: In real prediction markets, there can be fees, spreads, and slippage that eat into your edge. Take them into account when sizing bets.

- Chasing losses: Kelly assumes rational, independent bets. Emotional reactions such as doubling down after a loss break the model completely.

- Forgetting fractional Kelly: Full Kelly is mathematically optimal, but emotionally brutal. Fractional Kelly gives up a little theoretical gain for a huge boost in real-world survivability.

Summary

Kelly isn’t about winning every trade, but staying solvent long enough to let your edge pay off. So next time you find value in a prediction market, pause before trading and ask yourself: what’s my real probability here?”

Then use Kelly, preferably fractional, to guide your stake. You’ll be betting smarter, not harder, and your bankroll will thank you for it.

You may be interested in these articles: