Prediction markets have quietly gone from niche curiosity to serious financial assets. Yet for all the buzz around forecasting elections and conflicts, most participants never stop to think about who’s on the other side of their trade or why that matters.

A CEPR study found that market takers lose 32% on average, while makers lose around 10%, a staggering 22-point gap between the two roles. Knowing which role you play on a contract can have a meaningful impact on your returns.

In this article, we’ll go through:

- Overview of prediction markets and liquidity

- The market maker’s role in providing liquidity

- The market taker’s role in consuming liquidity

- Price discovery and platforms’ fee models

Definition of prediction markets and liquidity

In simple terms, prediction markets let participants buy and sell shares on the outcome of a real-world event. Each share pays out $1 if the event happens and $0 if it doesn’t, so the price of a share at any given moment reflects the crowd’s estimated probability. For instance, a contract trading at $0.65 implies a 65% chance the event happens.

As any market, the system only works if there’s enough liquidity, meaning there are always buyers and sellers ready to transact at a given price. Otherwise, the market would dry up and spreads blow out. That’s where the maker/taker distinction comes in, because these two roles are what keep liquidity flowing and prices ticking.

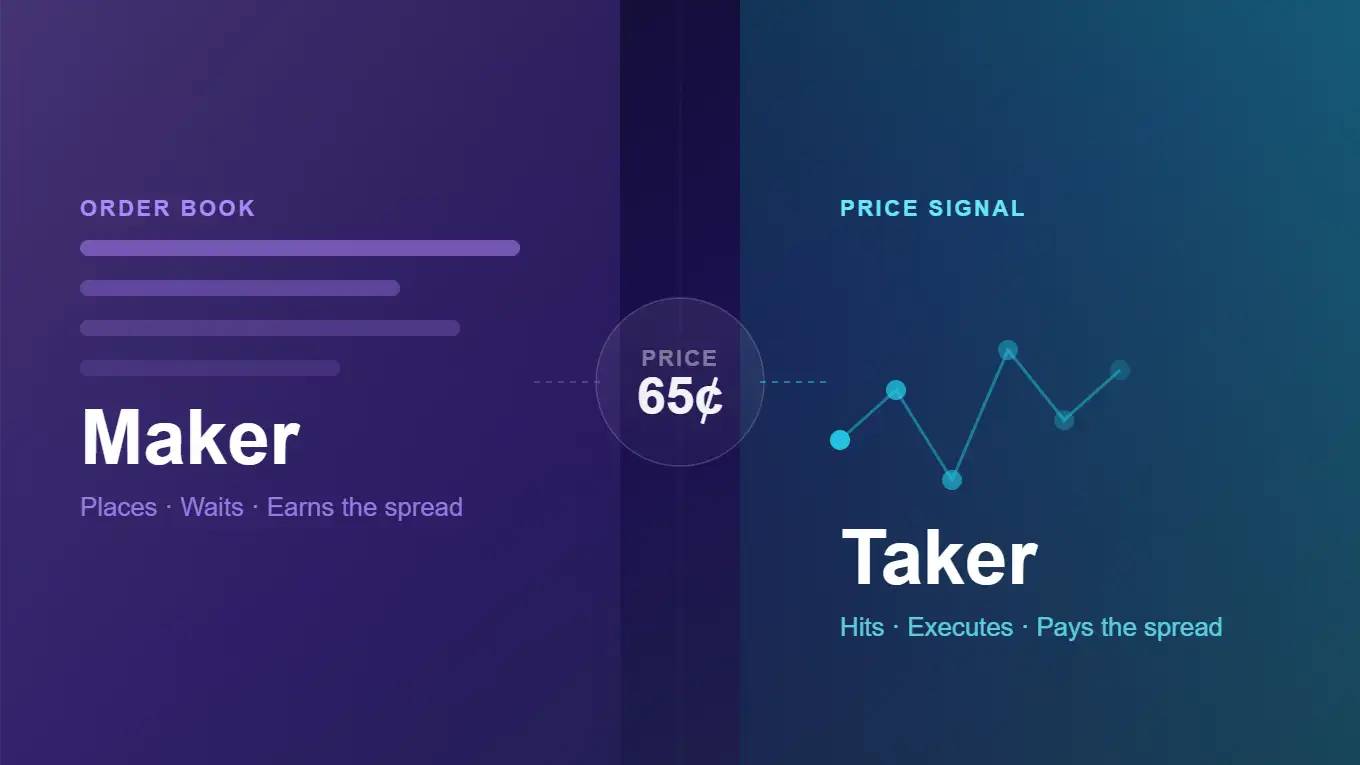

Role of the market maker

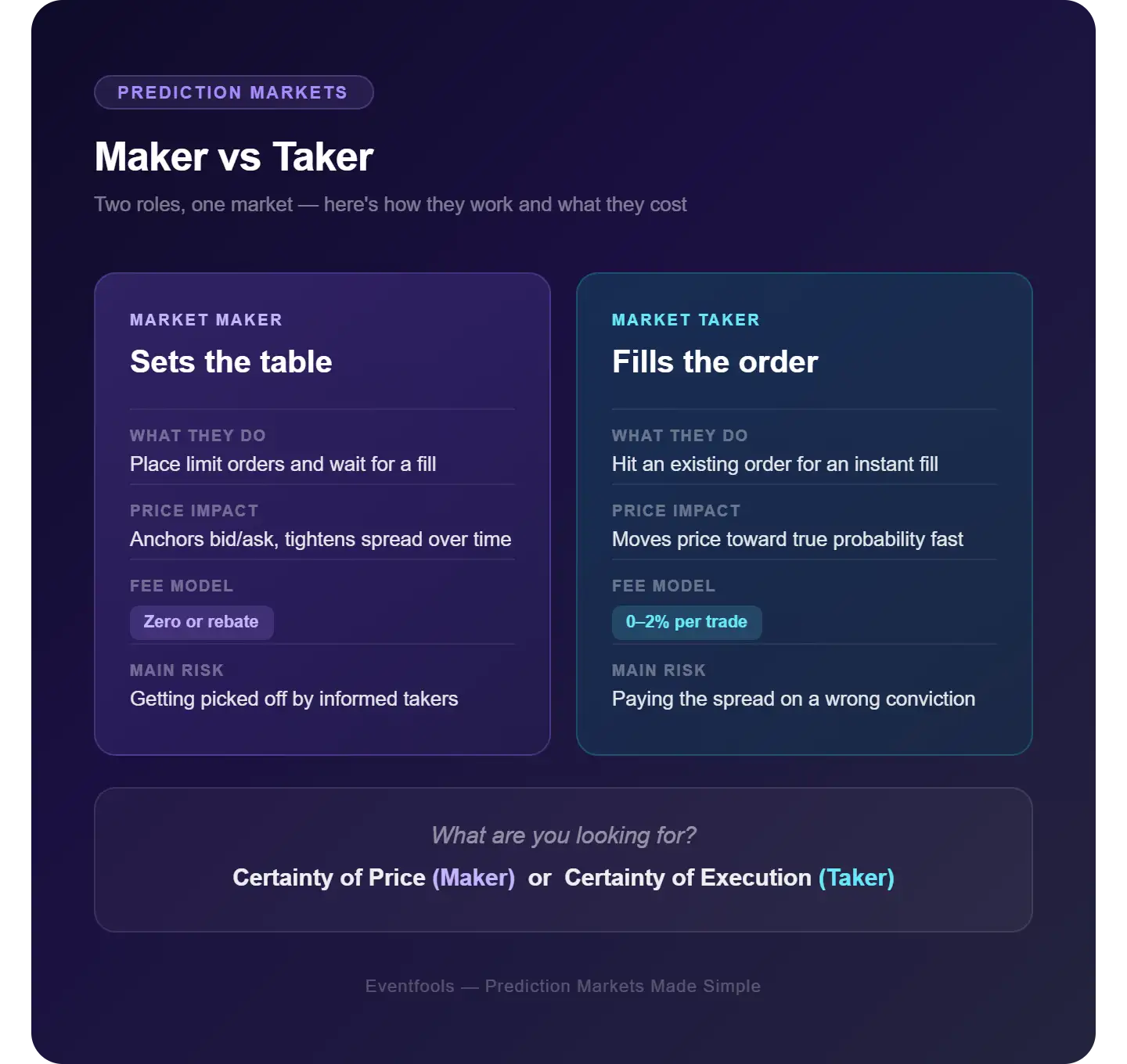

Market makers are the ones who show up early and set the table. Rather than jumping into an existing order, they place limit orders, offering to buy or sell at a specified price, and wait for someone else to fill them.

What do they get out of it? The spread, the difference between the bid price (buy) and the ask price (sell). It’s their compensation for taking on inventory risk and keeping the market open. On a thinly traded contract, that spread can be wide, but on a crowded geopolitical market, they will often narrow it down to fractions of a cent.

It’s worth pointing out that market makers aren’t just passive participants. They’re constantly adjusting their quotes as new information comes in, which is a reason why prediction market prices tend to respond quickly to breaking news.

Role of the market taker

If makers set the table, takers are the ones who sit down and eat. A market taker doesn’t post an order, but fills an existing one. They see a price on the book that works for them and take it immediately via a market order, paying the spread in the process.

Why would anyone willingly pay more or sell for less than the mid-price? Speed. Takers are usually acting on a conviction and don’t want to wait around for a limit order to get filled. The cost of missing the move outweighs the cost of the spread.

This urgency is what drives takers and it forces prices to move quickly in the process.

Price discovery and fees

Put these two roles together and you get a liquid market. Makers offer competitive quotes, takers fill them when they spot opportunities, and the back-and-forth pulls the market price toward true probability. As such, it aggregates information and conviction from thousands of participants.

Now, it’s worth noting that prediction platforms have built their fee structures around managing this maker-taker dynamic. For example, Kalshi and Polymarket both use tiered fee models that charge takers a percentage of their trade while offering rebates or zero fees to makers, a direct financial incentive to provide liquidity rather than consume it.

More specifically, Polymarket has charged taker fees in the range of 0-2% depending on market conditions, while makers often trade for free. The goal is to attract enough makers to keep spreads tight, which in turn attracts more takers, deepening the market for everyone. More liquidity means better prices, which brings in more participants.

Conclusion

The maker-taker split is the backbone of how financial markets work and prediction markets are no exception. Makers take on risk to keep things liquid and takers bring urgency and new information that keeps prices moving. Understanding which role you’re playing, and what you’re paying for, will make you a sharper participant in any market you trade on.

Frequently asked questions

What’s the difference between a maker and a taker in simple terms?

A maker adds liquidity to the market by placing a limit order at a set price. A taker consumes liquidity by filling that order. Makers set the price, takers accept it.

Do I have to choose one role, or can I be both?

You can be both. When you place a limit order, you’re acting as a maker. When you hit an order to get in or out quickly, you’re a taker. Most traders switch back and forth depending on their conviction and urgency.

Why do takers pay higher fees than makers?

Takers remove liquidity that someone else took the risk to provide. Platforms reward makers with lower or zero fees to encourage them to keep posting orders, since without them the market would grind to a halt.

Can anyone be a market maker on platforms like Polymarket or Kalshi?

Technically, yes by placing a limit order. But in practice, competitive market making on high-volume contracts is dominated by algorithmic traders and firms that can update quotes in real time.

What happens to a market when there aren’t enough makers?

Spreads widen, meaning the gap between the buy and sell price grows. This makes it more expensive to trade and less attractive to takers. In extreme cases, markets become illiquid and prices stop reflecting probability.

Is market making in prediction markets profitable?

It can be, but it comes with real risks. Makers can get caught on the wrong side of a sudden price move. Profitability usually comes down to how well a maker manages that adverse selection risk and how efficiently they update their quotes.

You may be interested in these articles: